Jumbo Loan Rates: What You Need to Know Before Applying

Jumbo Loan Rates: What You Need to Know Before Applying

Blog Article

Navigating the Complexities of Jumbo Lending Options to Find the Right Suitable For Your Needs

Browsing the complexities of big financing choices can be a needed however daunting action for those looking for to finance a high-value residential or commercial property. With a myriad of car loan types-- ranging from fixed-rate to interest-only and adjustable-rate-- each alternative offers unique benefits and possible risks. Understanding just how rate of interest prices and down repayment requirements rise and fall between these choices is crucial.

Understanding Jumbo Loans

A thorough understanding of jumbo car loans is important for browsing the complicated landscape of high-value realty funding. Unlike standard financings, jumbo car loans are developed for properties that exceed the Federal Housing Finance Company's adjusting car loan limits. These restrictions vary by area, showing regional genuine estate market conditions, yet commonly exceed $726,200 in the majority of locations since 2023. Such finances are important for acquiring high-end homes or buildings in high-cost areas where common financing fails - jumbo loan.

Jumbo finances entail distinctive underwriting standards, frequently needing a lot more rigorous credit report criteria. Borrowers are typically expected to demonstrate a durable credit history, typically 700 or higher, to certify. In addition, lending institutions usually mandate a reduced debt-to-income ratio, typically not surpassing 43%, to make sure the debtor can take care of the bigger financial commitment. A substantial deposit, generally ranging from 10% to 30%, is also a common requirement, reflecting the lender's raised risk direct exposure.

Passion rates on big finances may differ significantly, occasionally somewhat greater than those for conforming financings, because of the raised danger and absence of government support. Understanding these nuances is critical for customers intending to secure financing customized to high-value property deals.

Contrasting Car Loan Kinds

When considering high-value genuine estate funding, evaluating various car loan kinds comes to be an essential action in picking the most suitable choice for your economic demands. Jumbo car loans, commonly required for financing buildings that exceed conventional finance limits, come in different kinds, each with distinctive features tailored to particular customer accounts. Fixed-rate big car loans are frequently preferred for their predictability, offering a constant rates of interest and regular monthly settlement throughout the car loan period, which can relieve budgeting issues. This security is specifically appealing in a fluctuating economic environment.

Conversely, adjustable-rate big fundings (ARMs) provide first durations of lower rate of interest, usually making them an attractive choice for consumers that expect marketing or refinancing prior to the rate changes. The primary attraction here is the capacity for significant financial savings during the first fixed period, although they bring the risk of price increases gradually.

Interest-only jumbo lendings existing one more choice, allowing borrowers to pay only the passion for a given duration. This option can be beneficial for those looking for reduced preliminary settlements or who anticipate a considerable revenue increase in the future. Each funding kind has prospective downsides and distinct advantages, making mindful consideration important to straightening with long-term monetary methods.

Evaluating Rate Of Interest Prices

Rates of interest play an essential duty in determining the total cost of a jumbo loan, making their assessment a crucial part of the home loan option process. In the context of big lendings, which are not backed by government-sponsored entities and typically include higher amounts, rate of interest can differ more substantially than with adjusting car loans. This variation requires a complete understanding of just how rates are figured out and their lasting monetary effect.

The rate of interest on a big loan is influenced by a number of aspects, consisting of the loan provider's policies, market problems, and the debtor's credit reliability. Lenders normally examine the consumer's credit rating, debt-to-income proportion, and monetary books to set the rate. It's important for borrowers to compare prices from different lending institutions to ensure they protect the most desirable terms.

Dealt with and variable-rate mortgages (ARMs) supply different interest price frameworks that can affect payment security and overall funding costs - jumbo loan. A fixed-rate loan gives uniformity with foreseeable month-to-month repayments, whereas an ARM may use a lower first rate with prospective adjustments with time. Assessing these alternatives in the context of current rate of interest trends and personal monetary goals is critical for optimizing the cost-effectiveness of a jumbo loan

Assessing Deposit Requirements

Unlike standard finances, big financings typically require a higher down payment due to their dimension and threat account. Lenders often set the minimum down repayment for big finances at 20%, yet this can rise and fall based on factors such as credit report rating, lending amount, and the home's area.

The down payment not just influences the dimension of the funding however also influences the rates of interest and personal home loan insurance coverage (PMI) obligations. A bigger down settlement can lead to much more beneficial finance terms and possibly get rid of the need for PMI, which is usually called for when the deposit is less than 20%. Consequently, consumers must consider their financial capacity when check my blog figuring out the suitable deposit.

Furthermore, some loan providers might offer flexibility in deposit options if borrowers can demonstrate strong economic health, such as considerable cash books or an outstanding useful source credit background. Prospective jumbo lending consumers should thoroughly assess these variables to maximize their home loan method.

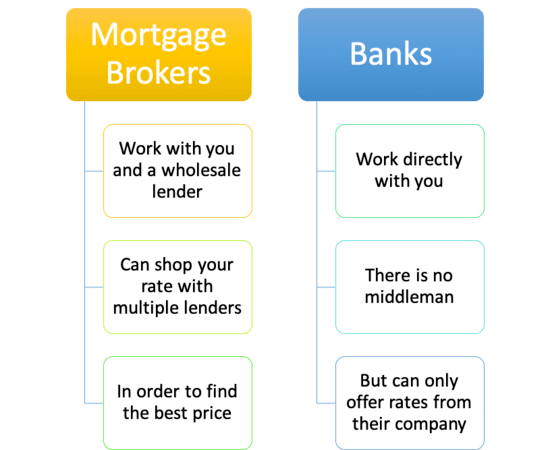

Picking the Right Lender

Choosing the ideal lending institution for a big financing is a pivotal choice that can significantly influence the terms and success of your home mortgage. Big loans, often exceeding the conforming loan limits, existing special difficulties and chances that necessitate careful factor to consider when picking a loaning partner. A lender's experience with jumbo loans, flexibility in underwriting, and competitive rates of interest are critical variables that ought to be thoroughly evaluated.

Developed loan providers with a background of successful jumbo lending handling can supply important understandings and smoother purchases. Because big car loans are not standard like standard lendings, a loan provider that supplies tailored services and items can much better align with your monetary objectives.

Compare multiple loan providers to determine affordable rate of interest rates and terms. A comprehensive comparison will empower you to make an educated choice, making sure that the picked loan provider supports your economic objectives successfully.

Conclusion

Navigating the intricacies of jumbo financing alternatives requires a comprehensive examination of funding types, rate of interest, and down repayment needs. A thorough assessment of economic situations, consisting of credit history and debt-to-income ratios, is critical in identifying the most proper funding type. In addition, picking loan providers with knowledge in big fundings can boost the likelihood of protecting desirable terms. Straightening funding features with long-lasting monetary objectives makes certain informed decision-making, eventually promoting the option of a financing that finest satisfies specific demands and scenarios.

Unlike conventional fundings, jumbo fundings are designed for properties that exceed the Federal Real estate Money Agency's adjusting funding limitations. Fixed-rate jumbo finances are typically favored for their predictability, offering a consistent passion price and monthly payment throughout the loan period, which can reduce budgeting problems. In the context of big finances, which are not backed by government-sponsored entities and frequently find out involve higher quantities, rate of interest rates can vary a lot more dramatically than with conforming fundings. Considering that jumbo lendings are not standardized like conventional loans, a lending institution that uses tailored services and items can better align with your financial objectives.

Report this page